Tuesday’s report on new dwelling profits arrived in as a overlook of estimates and prior revisions were all adverse. This information line confirms what we all know to be the circumstance: The housing market place, at least as it relates to development, is in a recession.

What I have normally tried using to do with my financial work is to connect the dots or exhibit a pathway to why anything could take place. Considering the fact that the summer time of 2020, I have truly thought the housing market could alter when the 10-calendar year yield broke in excess of 1.94%. Even so, for the new property gross sales sector, it would set their enterprise product at hazard.

We talked about this in March, and even past calendar year, when I wrote about the problem with the housing design increase premise. “I never count on a growth in housing building. Builders uncovered their lesson in the mid-2000s and understand that it is not in their ideal interst to make far more residential real estate over and above the typical need curve. They also uncovered their lesson rapidly in 2018 as home loan rates at 5% had been as well large for building development.”

Mortgage loan premiums have risen, and the builders have many homes underneath building, so they’re going to stall factors until eventually they know they can market their properties. This is why I raised the fifth economic downturn purple flag in June. In actuality, anything appears to be like normal as lengthy as you know that the builders never build households for society they make houses to make funds.

I dealt with this previous summer months in an short article titled: Why we cannot create our way out of a hot housing industry: “In the course of the past financial expansion from 2008 to 2019, the housing current market was subject to the regular refrain of establish more homes. Building a lot more households, it was said, would resolve all types of social issues, from creating homeownership additional affordable to ending homelessness.

“Today we are perhaps considerably less inclined to believing that a glut of new homes is the panacea modern society is waiting around for, but the siren get in touch with to make far more residences continues to be broadcast by a host of housing pundits and social do-gooders. The trouble with this scenario is that social do-gooders do not create households builders develop homes, and they construct households for dollars, not to get rid of societal ills.”

The preceding financial growth (2008-2019) had the weakest new house income restoration thus, we had the weakest housing design cycle ever. That tends to make sense to me builders missed profits estimates in 2013, 2014, and 2015. Then in 2018, they had a supply spike as mortgage rates achieved 5%. In reaction, they stalled building for 30 months. Right now, rates are even larger.

It is what it is: the housing predicament we stay with in America. If the builders need sub 4% mortgage loan rates to develop and existing residence price ranges are up near 20%, as Tuesday’s S&P CoreLogic Case-Shiller Dwelling Selling price Indices report showed, it’s really hard to see how we ever get out of this mess.

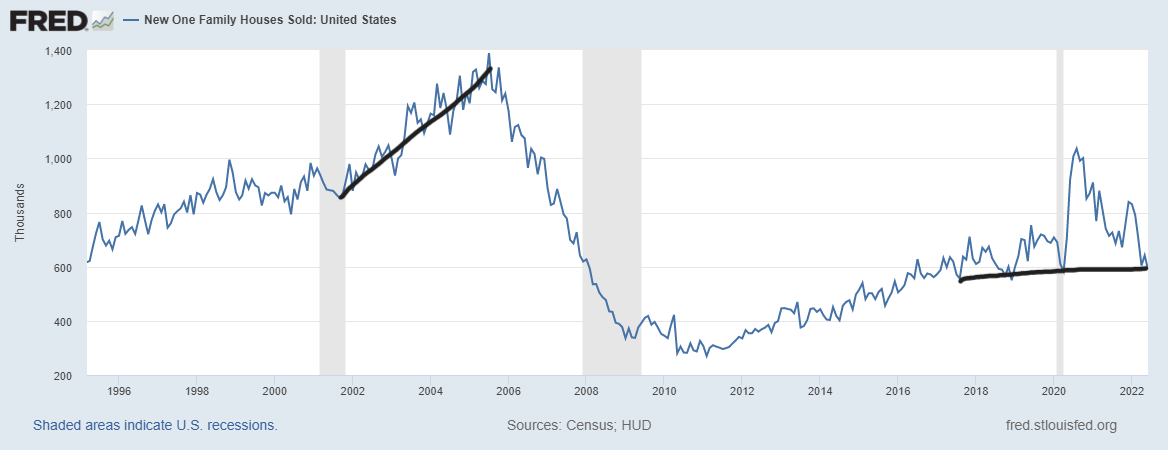

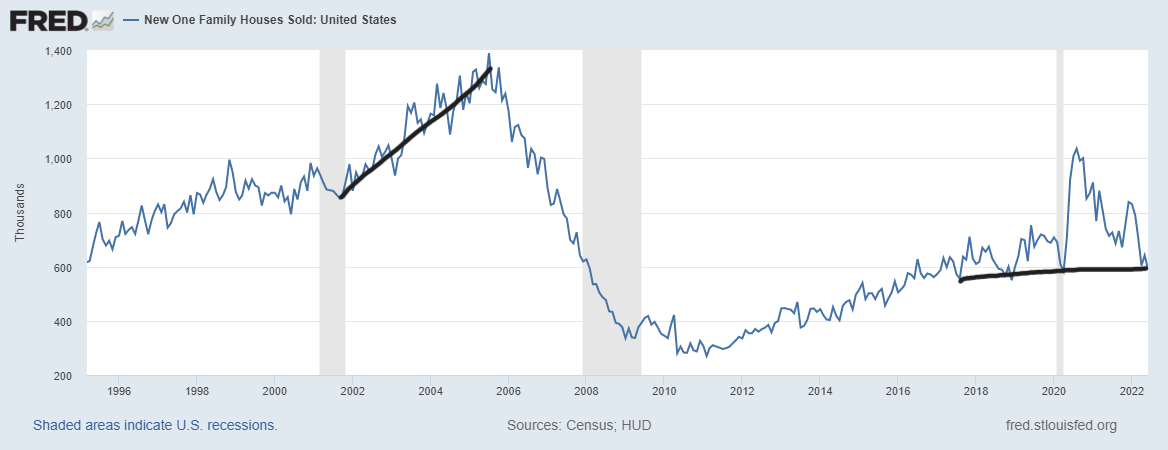

New dwelling product sales

From Census: Product sales of new single‐family homes in June 2022 have been at a seasonally altered yearly price of 590,000, in accordance to estimates launched jointly now by the U.S. Census Bureau and the Section of Housing and Urban Advancement. This is 8.1 p.c (±15. %)* below the revised May perhaps rate of 642,000 and is 17.4 per cent (±11.6 per cent) under the June 2021 estimate of 714,000

These days, new dwelling profits are back to 2018 concentrations. The peak of the housing bubble was around 1.4 million in sales. At today’s degree of 590,000 homes, the builders are in a various place to offer with their inventory challenges due to the fact they haven’t had a credit history profits increase as we saw from 2002-2005. We are effortlessly below the 2000 economic downturn concentrations and back to 1996 amounts in demand. Builders will deal with their design houses to ensure they don’t have as well much product or service. Also, they are hoping for lessen home finance loan fees, which helped them out in 2019.

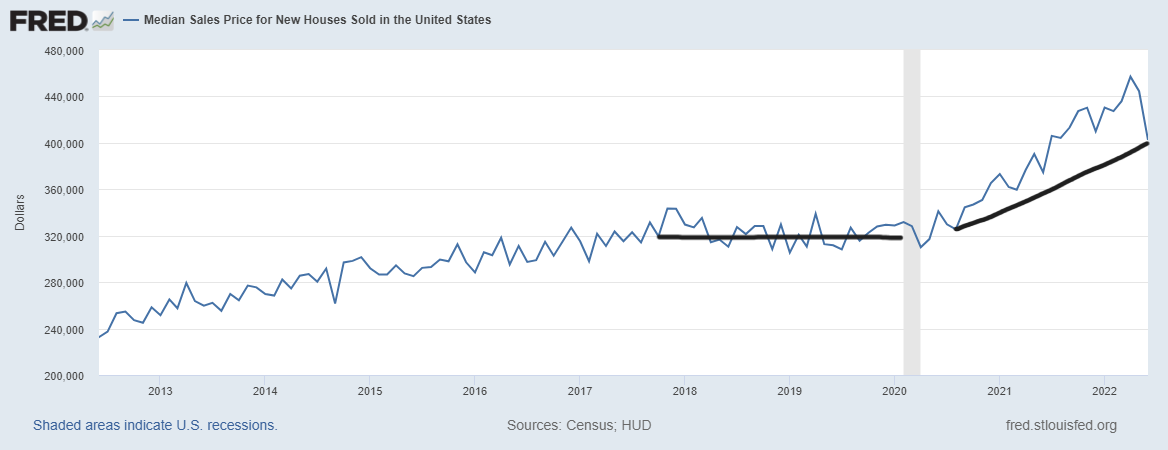

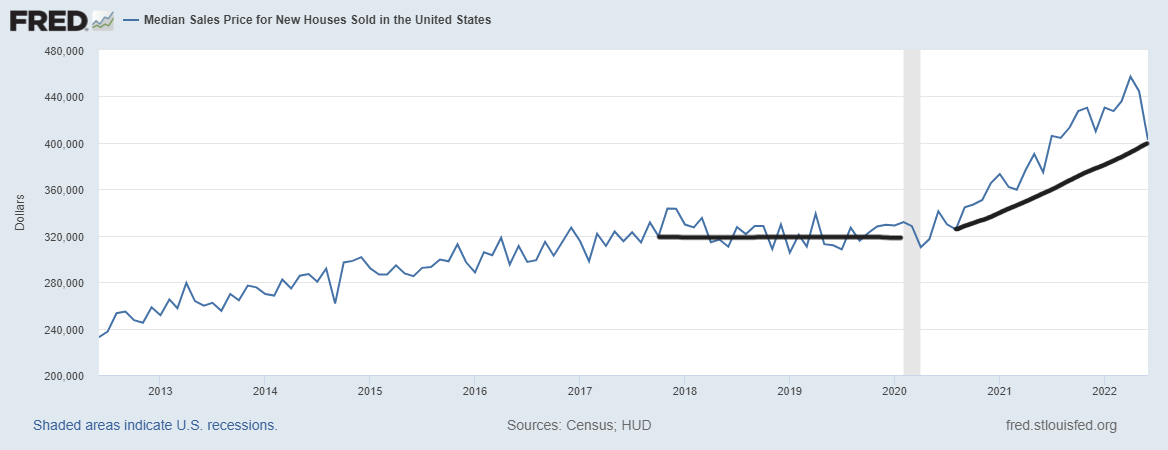

Census: The median sales rate of new properties sold in June 2022 was $402,400. The regular profits cost was $456,800.

There’s a savagely unhealthy housing current market concept here, and my problem is home price ranges overheating, which can impact the housing sector a lot more than if price expansion ended up steady. The incredibly hot property cost bash started out in 2020, which was not great. The builders had pricing energy and employed it well for earnings margins. The client had to fork out the price tag. This is how provide and demand from customers functions the one point that can transform pricing electrical power is higher fees.

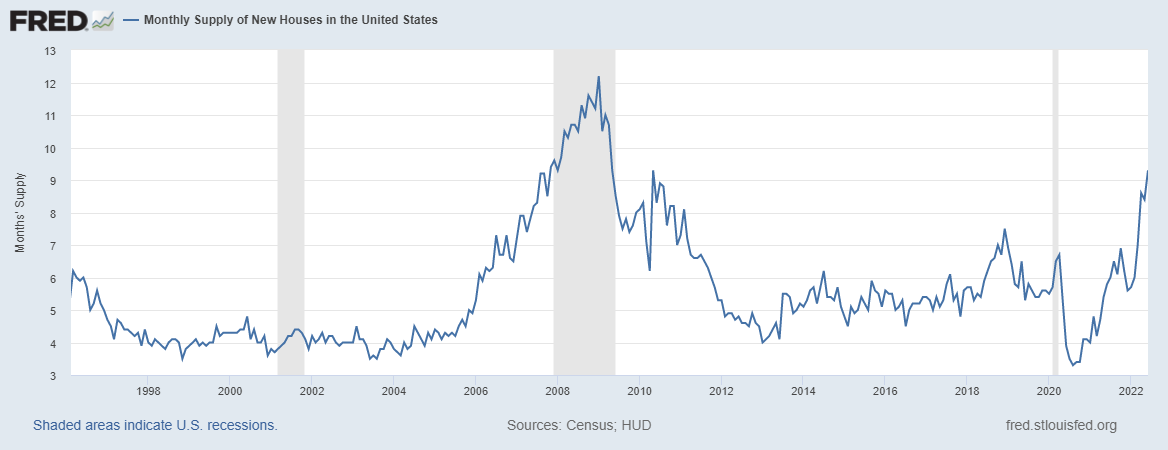

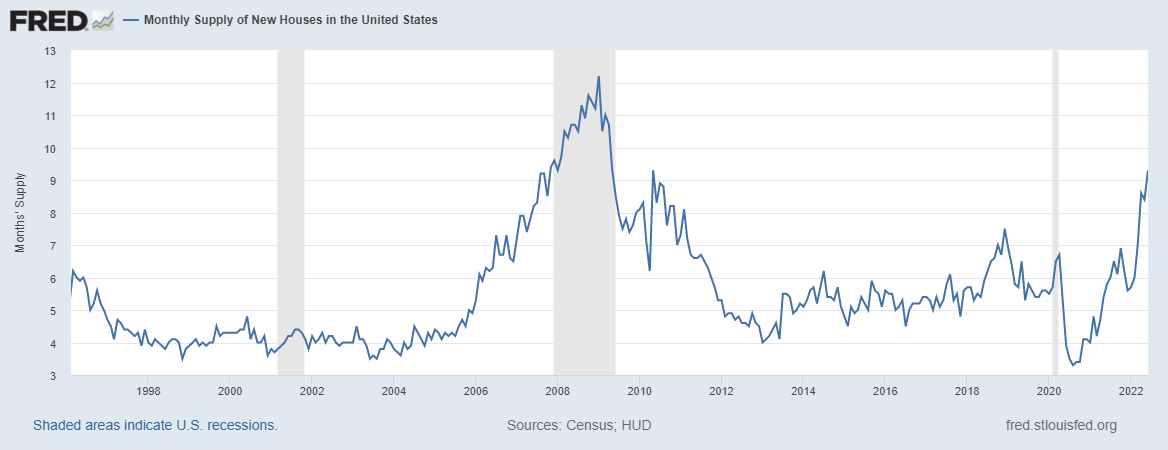

From Census: The seasonally‐adjusted estimate of new properties for sale at the conclusion of June was 457,000. This signifies a source of 9.3 months at the existing gross sales level.

My rule of thumb for anticipating builder habits is based mostly on the a few-thirty day period regular of offer:

- When provide is 4.3 months and down below, this is an great sector for the builders.

- When offer is 4.4 to 6.4 months, this is an Ok current market for the builders. They will create as very long as new home sales are developing.

- The builders will pull back on design when the supply is 6.5 months and higher than.

As we can see down below, the every month provide has taken off as soon as once more. The builder’s business model is at risk, of study course.

Even so, we should be mindful of one particular actuality that is unique from the earlier: Only .83 months of offer is finished housing solution.

- 6.22 months of provide is less than design

- 2.24 months of supply has not even been started still

We should really count on that builders won’t even convey a shovel to the filth of the residences they haven’t began on but — and they will gradual the procedure down to make sure the properties under construction will be sold. In the earlier, reduced mortgage rates have assisted this course of action out for them, so they know what they are doing in this article. As we can see, like everything with housing, absolutely nothing in 2022 looks like 2008.

This is the builder’s most important competitiveness. They have taken benefit of the minimal stock tale in 2020 and 2021.

NAR: Whole Stock Facts

2007 Peak Approximately 4,000,0000

2022 1,260,000

I am not a housing building increase human being this market has boundaries. The new dwelling product sales sector and housing starts off will grind items out till house loan fees go decreased and they can provide a lot more product and truly feel at ease constructing properties yet again. Until eventually that time frame, it’s absolutely nothing but a savagely unhealthy housing marketplace.